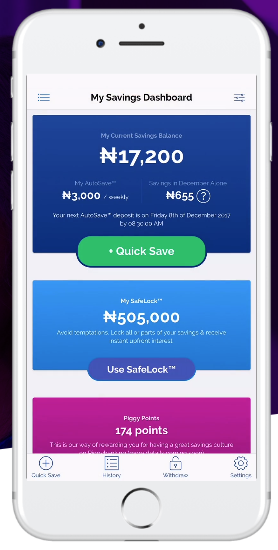

Seeking to tap into Africa’s informal savings groups the Nigerian investment startup Piggybank.ng closed $1.1M in seed funding and announced a new product — Smart Target, which offers a more secure and higher return option for Esusu or Ajo group savings clubs common across West Africa.

The financing was led with a $1 million commitment from LeadPath Nigeria, with Village Capital and Ventures Platform contributing $50,000 each.

Founded in 2016, Piggybank.ng offers online savings plans — primarily to low and middle income Nigerians — for deposits of small amounts on a daily, weekly, monthly, or annual basis. There are no upfront fees.

Savers earn interest rates of between 6 to 10 percent, depending on the type and duration of investment, Piggybank.ng’s Somto Ifezue told TechCrunch in Lagos with co-founders Odunayo Eweniyi and Joshua Chibueze.

Users need an account with one of PiggyBank.ng’s bank partners to use the products. The startup generates returns for small-scale savers (primarily) through investment in Nigerian government securities, such as bonds and treasury bills.

PiggyBank.ng generates revenue through asset management and from the float its balances generate at partner banks.

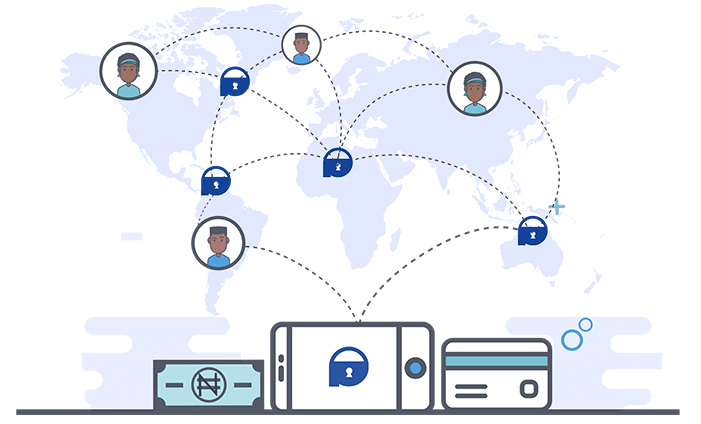

The startup looks to grow clients across younger Nigerians and the country’s informal saving groups.

“The market that we are trying to serve is largely the millennial market, though we do not exclude anyone,” said Eweniyi, the company’s chief operating officer. The venture also looks to meet a demand in Nigeria for accessible investment options, citing a survey they conducted indicating that as a top priority for people with discretionary income.

“Piggybank offers savings, but our vision is not just savings, but to become a holistic platform — a financial warehouse — where other financial providers can plug in their services for PiggyBank users,” said Eweniyi. She cited banks, investment houses, insurance, and pension funds as possible partners.

The company currently has 53,000 registered users — 60 percent of whom are Nigerian Millennials — who have saved in excess of $5M since 2016, according to a release.

PiggyBank.ng will use its $1.1M in new seed funding for “license acquisition and product development.”

The startup has taken preliminary steps to launch in other African countries (Kenya in particular) but could not offer exact details.

Groups will be able to choose savings options and goals through PiggyBank.ng’s app and receive automated disbursement of returns across their individual bank accounts, according to COO Eweniyi.

As for how the company assures savers it won’t become another Ponzi scheme, Piggybank.ng and its lead investor point to the startup’s pending banking license with Nigeria’s Central Bank. The company is in the process of acquiring a micro-finance banking license, something LeadPath Nigeria founder Olumide Soyombo confirmed on a call with TechCrunch. He also pointed to Piggybank’s client balances being held with registered banks, which are protected under Nigeria’s own FDIC type banking insurance.

Soyombo will take a role on Piggybank.ng’s board and he’d like to see them open up new options for individuals to input money on the platform. “The agent network business is a huge play we plan to go into. They’ve basically become like human ATMs,” Soyombo said. He referenced Nigerian digital payment company Paga and Safaricom’s M-Pesa with large agent network stations where clients can fund digital accounts with cash.

While digital payments products have caught on in certain parts of Africa, E-Trade type citizen investment platforms have yet to emerge at any scale.

Soyombo doesn’t see Piggybank.ng moving from fixed income investments to equities just yet. “Maybe down the line stocks could be an interesting play, but not right now. People are currently looking for a more risk free place to e-tail,” he said.

Soyombo believes Piggybank.ng has the potential to become an acquisition target.

“They usually only happen in our market with two main players: banks and telcos,” he said. “The banks have been slow to try new things in this savings space. Piggybank is coming in…and filling a particular need, so they are in a very acquisitive space.”

from TechCrunch https://ift.tt/2xtv3Oz

No comments:

Post a Comment